The ATO has set its sights on distributions of trust income to adult children.

Trustees should review their circumstances where they have distributed trust income to adult children to take advantage of lower marginal tax rates and some other person has obtained the actual benefit of that trust income. That other person may be other beneficiaries (e.g. mum and dad) or the trustee of the trust.

The ATO has published guidance on when they consider arrangements will be OK (green zone), not OK (red zone) or require further investigation (blue zone).

What is section 100A?

Section 100A is an anti-avoidance provision.

Historically, section 100A was introduced to deal with a scheme known as ‘trust stripping’. This generally involved a beneficiary with special tax characteristics (e.g. losses or an income tax exempt status) being introduced to the controllers of a discretionary trust that was earning trust income. The trust income was then distributed to the introduced beneficiary, but that income was then ‘reimbursed’ back to the trustee or its controllers.

When section 100A applies, the trustee is taxed on the trust income at the top marginal rates.

Despite the reason for the section being introduced, the cases acknowledge that section 100A applies more broadly than just to trust stripping cases.

The ATO has turned its attention to distributions of trust income to adult children on lower marginal tax rates where some other person has obtained a benefit attributable to that trust income.

What are the elements of section 100A?

The elements in section 100A are technical, and draw on old case law. However, in very broad terms, section 100A applies when:

- a beneficiary is made presently entitled to trust income

- there was an arrangement that another person (usually another beneficiary or the trustee) gets a benefit attributable to that trust income – this is called a ‘reimbursement agreement’

- a purpose of the arrangement was someone paying less tax

- the arrangement was not an ‘ordinary family or commercial dealing’.

The ATO view is that an arrangement is an ‘ordinary family or commercial dealing’ when what has happened can be readily explained by family or commercial objects. If what has happened is only explicable by tax reasons, the exception for ‘ordinary family or commercial dealings’ will not apply.

In one ATO example, a trust is created under a Will. An adult child who is 18 is made presently entitled to all of the trust income, but that income is not to be paid until the child turns 25. The trustee reinvests the income in the meantime. That arrangement is explained by ordinary family objectives. It is not caught by section 100A even if the other conditions are satisfied.

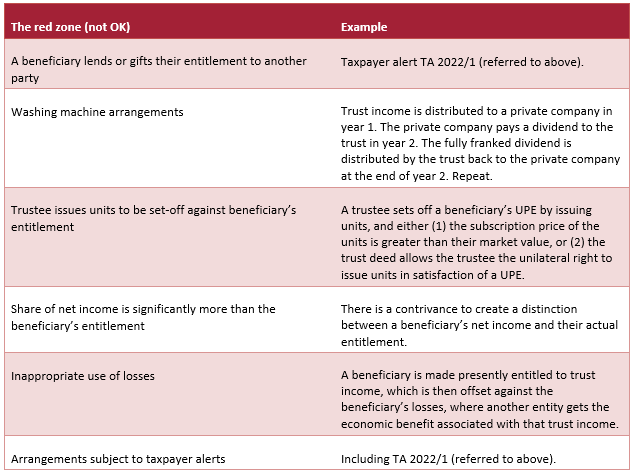

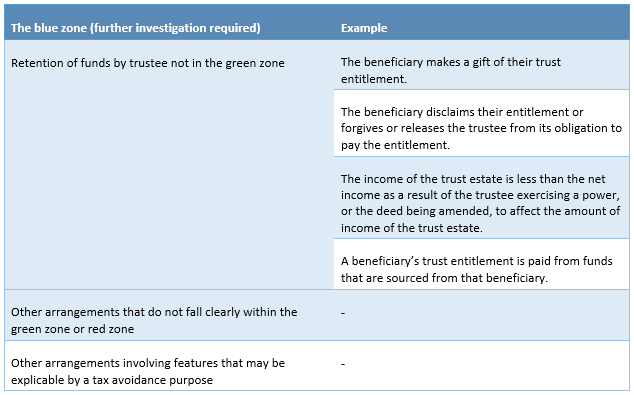

We have set out some of the other examples raised by the ATO in the tables below.

Is the ATO coming to audit me?

It depends.

The ATO has a particular issue with an arrangement where:

- trust income has been distributed to adult children on lower marginal tax rates

- the parents have the benefit of that trust income

- the adult children are never paid that trust income because their parents say:

-

- the adult children have to pay back their parents the costs of raising them as a child

- the adult children have to meet their share of family costs (which is higher than actual costs)

- there is an agreement that the parents will manage all of the pooled family members’ entitlements.

This arrangement is subject to a taxpayer alert – TA 2022/1.

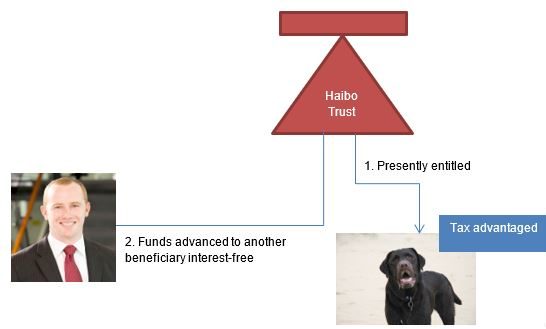

This is only one example of an arrangement in the red zone. Take the following example where Haibo is made presently entitled to Haibo Trust’s income, which is offset against his losses. However, the funds are advanced to Fletch, who gets the economic benefit associated with the trust income.

There are other arrangements that the ATO say may trigger section 100A, set out in the tables below.

How far back are we looking?

Alarmingly, there is no amendment period for section 100A assessments.

However, the ATO has indicated that in most cases it will not look back to the 2014 and earlier income years. There are some exceptions to this.

What arrangements are in what zones?

How should I deal with existing entitlements?

First, it is important to remember that the ATO’s tables set out a compliance approach. According to the ATO, items in the red zone and blue zone warrant an ATO review – with red zone a higher priority than blue zone.

However, depending on the specific facts, arrangements in the blue zone or red zone may not trigger section 100A.

Second, the items described in the tables help identify whether there is a risk that section 100A applies to an arrangement. The actual legal test of whether section 100A applies depends on whether there was a reimbursement agreement at the time the beneficiary was made presently entitled to the trust income. For example, a beneficiary may release the trustee from its obligation to pay an entitlement in five years’ time (and fall within the blue zone). If that release was not part of an arrangement at the time the beneficiary was made presently entitled to its trust income, it is not part of a ‘reimbursement agreement’ under section 100A.

The best next steps will often be:

- identifying the actual level of risk of section 100A applying based on your particular circumstances

- depending on the outcome of step 1, identifying the best options for dealing with any existing or historical risks.